Medicare is the federal health insurance program for people over 65 and those with certain disabilities. Medicare Advantage is a version of Medicare run by private insurance companies that contract with the government. These plans typically offer extra benefits, such as dental, vision and prescription drug coverage, that aren’t included with traditional Medicare. More than half of eligible Medicare beneficiaries now get their coverage through private Medicare Advantage plans.

But this year, as Medicare’s open enrollment season kicks off, more than 1 million patients will have to shop for new health insurance. Facing financial and federal regulatory pressures, many insurers are pulling their Medicare Advantage plans from counties and states they’ve deemed unprofitable. Meanwhile, large health systems in states including Alabama, Minnesota and Vermont have cut ties with some Medicare Advantage plans.

It’s a situation that’s alarmed state insurance regulators, who are fielding questions from older adults concerned about their hospitals and doctors withdrawing from their Medicare Advantage plans. Last month, the National Association of Insurance Commissioners sent a letter to the federal Centers for Medicare & Medicaid Services asking for guidance.

“Beneficiaries are faced with either paying the increased out-of-network costs or rescheduling their necessary medical services with another provider who may not have prompt availability,” the insurance commissioners’ group wrote. “A delay in access to medically necessary services is likely to result in harm.”

Complete Article

americanmilitarynews.com

americanmilitarynews.com

But this year, as Medicare’s open enrollment season kicks off, more than 1 million patients will have to shop for new health insurance. Facing financial and federal regulatory pressures, many insurers are pulling their Medicare Advantage plans from counties and states they’ve deemed unprofitable. Meanwhile, large health systems in states including Alabama, Minnesota and Vermont have cut ties with some Medicare Advantage plans.

It’s a situation that’s alarmed state insurance regulators, who are fielding questions from older adults concerned about their hospitals and doctors withdrawing from their Medicare Advantage plans. Last month, the National Association of Insurance Commissioners sent a letter to the federal Centers for Medicare & Medicaid Services asking for guidance.

“Beneficiaries are faced with either paying the increased out-of-network costs or rescheduling their necessary medical services with another provider who may not have prompt availability,” the insurance commissioners’ group wrote. “A delay in access to medically necessary services is likely to result in harm.”

Complete Article

1 million+ patients lose coverage as insurers, hospitals drop Medicare Advantage

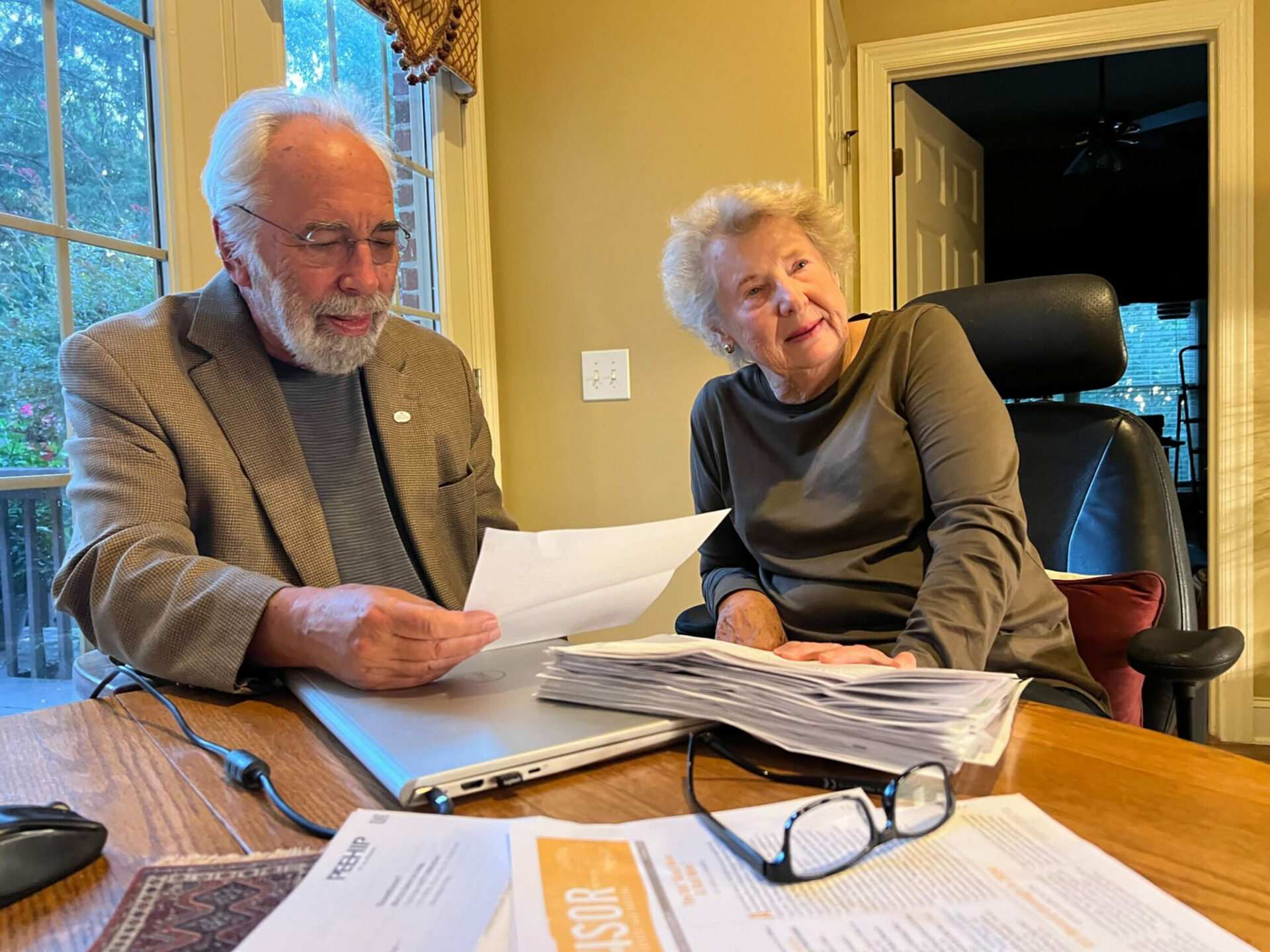

Libby and Andrew Potter usually ignore the avalanche of Medicare Advantage ads that land in the mailbox at their home in Huntsville, Alabama, each fall as

americanmilitarynews.com